India’s BioCNG Market Moves from Policy to a Cautious, Structured Scale

By Ivys Adsorption

India’s biomethane sector is transitioning to a structured scale-up, supported by multi-ministry policy alignment and a growing pipeline of small-to-mid-scale projects.

India’s BioCNG (compressed biogas) market is entering a new phase of development, moving cautiously but in a structured manner across sectors. While the SATAT initiative (Sustainable Alternative Towards Affordable Transportation) and MoPNG (Ministry of Petroleum & Natural Gas) initially catalyzed market formation, momentum today reflects a broader policy framework. MoPNG is advancing demand creation through blending mechanisms, while the GOBARdhan programme (Galvanizing Organic Bio-Agro Resources Dhan) and the Ministry of Jal Shakti focus on feedstock aggregation, plant registration, waste-to-value outcomes, and support provided through MNRE’s (Ministry of New and Renewable Energy) waste-to-energy schemes. All three public-sector oil marketing companies, Indian Oil, Bharat Petroleum, and Hindustan Petroleum, have formed partnerships under SATAT with private developers to procure BioCNG and help scale project deployment. Together, these measures position biomethane as an emerging component of India’s regulated gas ecosystem.

India’s BioCNG (compressed biogas) market is entering a new phase of development, moving cautiously but in a structured manner across sectors. While the SATAT initiative (Sustainable Alternative Towards Affordable Transportation) and MoPNG (Ministry of Petroleum & Natural Gas) initially catalyzed market formation, momentum today reflects a broader policy framework. MoPNG is advancing demand creation through blending mechanisms, while the GOBARdhan programme (Galvanizing Organic Bio-Agro Resources Dhan) and the Ministry of Jal Shakti focus on feedstock aggregation, plant registration, waste-to-value outcomes, and support provided through MNRE’s (Ministry of New and Renewable Energy) waste-to-energy schemes. All three public-sector oil marketing companies, Indian Oil, Bharat Petroleum, and Hindustan Petroleum, have formed partnerships under SATAT with private developers to procure BioCNG and help scale project deployment. Together, these measures position biomethane as an emerging component of India’s regulated gas ecosystem.

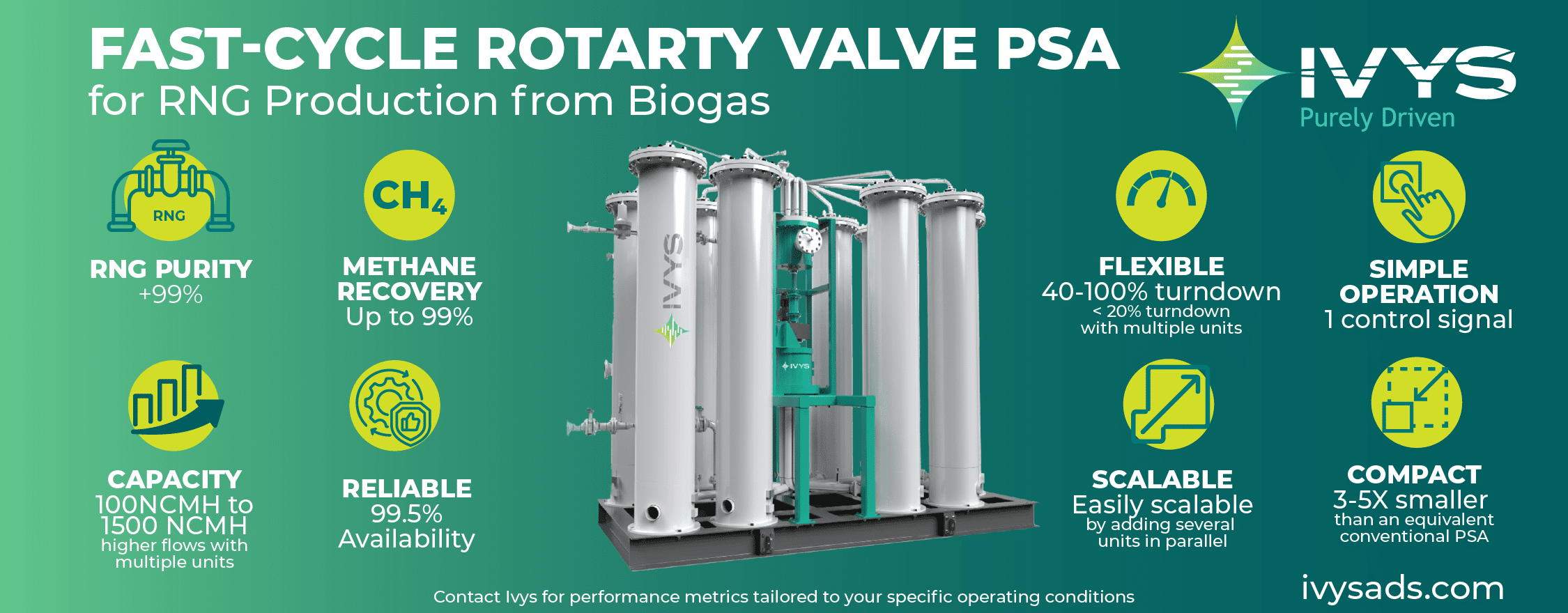

In this market context, Ivys Adsorption is advancing its pressure swing adsorption (PSA) technology for biomethane upgrading applications in India. Ivys’s fast-cycle rotary-valve PSA systems, designed for rapid modular deployment, are gaining traction due to its competitive total cost of ownership (TCO) across the sugar, paper, agricultural residue, and dairy sectors. This year, 2026, Ivys will supply and commission its PSA systems for five to six BioCNG projects across India, growing its presence from several existing plants. Project developers are choosing Ivys’s PSA for their robustness, low operating costs and ease of operation. Ivys is also growing its presence in select Southeast Asian markets as well.

India’s organic-waste resource can support approximately 85–90 billion cubic metres per year, equivalent to more than 3 billion MMBtu annually of BioCNG production, as cited by IOCL and multiple national studies. Independent analysts size the market at USD 1.5–1.7 billion in 2024, with projections of USD 3.5–5 billion by 2030–32, implying a ~20% CAGR. Project development reflects this diversity, with activity concentrated in sugar press-mud digesters, dairy manure clusters, municipal organic waste facilities, and agricultural waste projects, most commonly in the 5–25 tonnes per day range. India’s CBG Blending Obligation requires CGD entities to blend 1% CBG into CNG/PNG in 2025–26, rising to 3–5% thereafter, creating assured offtake via city gas and CNG stations. CGD–CBG synchronization schemes enable grid injection or trucked supply under energy-linked contracts, operationalizing this demand.

You can find more insights like this in the 2026 Asia Edition of the Biogas Community Magazine.

Comments